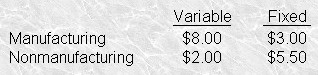

题干:Mill Corporation在最近的会计年度内单位成本如下,Mill Corporation的存货1月1日是6k,12月31日是5.2k,与可变成本法相比,吸收成本法下利润是

考点:Cost Allocation Techniques-Absorption and Variable Costing -- Calculations

关键词:absorption costing income

解题思路:

在吸收成本法中,固定制造费用是产品成本的一部分。在变动成本法中,产品的成本不

包括固定制造费用。

在吸收成本法中,固定制造费用分摊到销货成本和存货中,反映在存货中的部分不会进

入当期损益,而在变动成本法中,固定制造费用作为期间费用,全部进入当期损益。

在吸收成本法中,财务报表的格式是毛利格式,突出了制造成本和非制造成本的区别;

在变动成本法中,财务报表是边际贡献格式,突出了固定成本和变动成本的区别。

所以可变成本法和吸收成本法利润区别就在于期末存货和期初存货差异中的固定费用部分。

Answer (A) is correct . The difference in operating income between the absorption-costing basis and the variable-costing basis can be calculated as the difference between the ending inventory in units and the beginning inventory in units (6,000 – 5,200 = 800), multiplied by the budgeted fixed manufacturing cost per unit ($3), for a total difference of $2,400. Since absorption costing treats fixed overhead as a period cost and variable costing embeds it in ending inventory, operating income under absorption costing will be lower.

Answer (B) is incorrect because If there is a balance in either beginning or ending inventory, operating income will be lower under absorption costing than under variable costing.

Answer (C) is incorrect because The amount of $6,800 results from multiplying the difference in beginning and ending inventory by all fixed costs rather than by only fixed manufacturing cost.

Answer (D) is incorrect because The amount of $6,800 results from multiplying the difference in beginning and ending inventory by all fixed costs rather than by only fixed manufacturing cost; also, if there is a balance in either beginning or ending inventory, operating income will be lower under absorption costing than under variable costing.