微信扫一扫

实时资讯全掌握

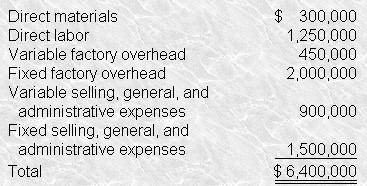

A company has just completed the final development of its only product, general recombinant bacteria, which can be programmed to kill most insects before dying themselves. The product has taken 3 years and $6,000,000 to develop. The following costs are expected to be incurred on a monthly basis for the normal production level of 1,000,000 pounds of the new product:  At a sales price of $5.90 per pound, the sales in pounds necessary to ensure a $3,000,000 profit the first year would be (to the nearest thousand pounds) At a sales price of $5.90 per pound, the sales in pounds necessary to ensure a $3,000,000 profit the first year would be (to the nearest thousand pounds)A. 13,017,000 pounds. B. 14,000,000 pounds. C. 15,000,000 pounds. D. 25,600,000 pounds. |