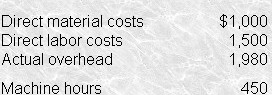

Answer (B) is correct . The results from the production run of 1,000 units allow Baldwin to calculate its per-unit costs for materials ($1,000 /1,000 units = $1.00) and labor ($1,500/ 1,000 units = $1.50).

Overhead can then be derived as follows: Total cost per unit $4.30 Less:direct materials (1.00) Less:? direct labor (1.50) Overhead per unit $1.80 The number of machine hours required to manufacture a single unit is .45 (450 hours/ 1,000 units). Therefore, $1.80 represents 45% of the cost of a machine hour ($1.80/0 .45 = $4.00). Since 150,000 hours were budgeted, total budgeted overhead for the year was $600,000 (150,000 hours*$4.00 per hour)

Answer (A) is incorrect because The amount of $577,500 results from treating the .45 units per hour ratio as a cost, deducting it from the total unit cost, then improperly multiplying this total unit cost by the budgeted total machine hours.

Answer (C) is incorrect because The amount of $645,000 results from simply multiplying total unit cost by the budgeted total machine hours.

Answer (D) is incorrect because The amount of $660,000 results from allocating overhead based on actual rather than budgeted usage.