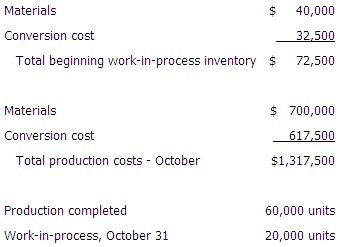

题干:奥斯特制造采用的是加权平均的过程的成本核算系统,以下是十月份期间成本和活动信息

所有材料都在制造过程的开始一次性投入,并转换成本在整个生产均匀地发生。与工厂人员对话表明,平均而言,月末在制品库存为25%完成。假设没有损耗,应如何分配奥斯特的10月份制造业成本?

考点:Cost Accumulation Systems-Process Costing

关键词:WIP FG WAC

解题思路:本题目应算出加权平均下约当量

原材料加权成本=40+700=740

转换成本=32.5+617.5=650

原材料约当量=80

转换成本的约当量=60+20*0.25=65

WIP成本=20*740/80+5*650/65=235

FG成本=740+650-235=1155

This is an allocation of only the costs added during the month. It does not include the costs in beginning work-in-process inventory.

Total materials cost to be allocated under the weighted average method is $40,000 in beginning WIP + $700,000 added during the month = $740,000. Total conversion cost to be allocated under the weighted average method is $32,500 in beginning WIP + $617,500 added during the month = $650,000. For direct materials, the total number of equivalent units using the weighted average method was 60,000 units completed plus the 20,000 (100% complete) units in ending WIP inventory, for a total of 80,000 equivalent units. The units in ending WIP inventory are 100% complete as to direct materials because all materials are introduced at the start of the manufacturing process. For conversion costs, the total number of equivalent units under the weighted average method was 60,000 units completed plus the 5,000 equivalent units (20,000 units, 25% complete) to start ending work-in-process inventory, for a total of 65,000 equivalent units. The costs per equivalent unit are: Direct materials: $740,000 ÷ 80,000 EUP = $9.25. Conversion costs: $650,000 ÷ 65,000 EUP = $10.00. The costs of the completed units are: Direct materials: $9.25 × 60,000 = $555,000 Conversion costs: $10.00 × 60,000 = $600,000 Total costs of completed units: $555,000 + $600,000 = $1,155,000 The costs in ending work-in-process inventory are: Direct materials: $9.25 × 20,000 = $185,000 Conversion costs: $10.00 × 5,000 = $50,000 Total costs of units in ending work-in-process inventory: $185,000 + $50,000 = $235,000

This was calculated using 80,000 as the total equivalent units of production for both direct materials and conversion costs, which is the total of the number of units completed plus the number of units in ending work-in-process inventory. This does not take into consideration the state of completion of the ending work-in-process inventory.

This was calculated using 65,000 as the total equivalent units of production for both direct materials and conversion costs. That is the total of the number of units completed plus the number of equivalent units for conversion costs in ending work-in-process inventory based on 25% completion. The number of equivalent units for direct materials in ending work-in-process inventory is different, because the materials are added at the start of the process.