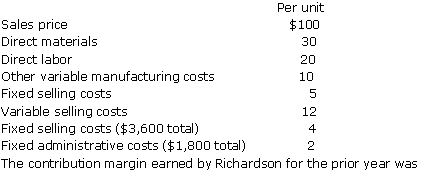

A. Contribution margin is calculated as revenues minus variable costs. Unit contribution margin is sales price minus unit variable costs, or $28 per unit ($100 - $30 - $20 - $10 - $12). There were 900 units sold, so the total contribution margin is $25,200 ($28 × 900).

B. This answer results from three errors: (1) using the number of units produced instead of the number of units sold; (2) subtracting all manufacturing costs, including fixed manufacturing costs, from sales. Fixed manufacturing cost is not subtracted from sales to calculate the contribution margin; and (3) not subtracting variable costs other than variable manufacturing costs from sales to calculate the contribution margin. Variable costs other than variable manufacturing costs are included in the items subtracted from sales to calculate the contribution margin.

C. This answer incorrectly uses the number of units produced instead of the number of units sold. See the correct answer for a complete explanation.

D. This answer results from two errors: (1) subtracting all manufacturing costs, including fixed manufacturing costs, from sales. Fixed manufacturing cost is not subtracted from sales to calculate the contribution margin; and (2) not subtracting variable costs other than variable manufacturing costs from sales to calculate the contribution margin. Variable costs other than variable manufacturing costs are included in the items subtracted from sales to calculate the contribution margin.