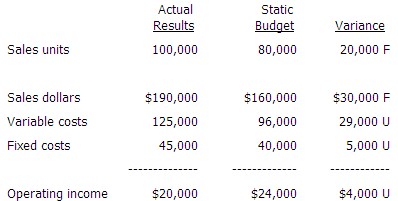

题干:下列是Dale公司4月份信息

在弹性预算下,Dale总共销售数量差异是

考点:Cost and Variance Measures-Variance Analysis Overview

关键词:volume

解题思路:sales volume vavriance=单位边际贡献*(实际销量-预算销售量)

本期CM=(24000+40000)/80000=0.8

那么差异=0.8*20000=16000 有利差

This is the total flexible budget variance, or actual operating income minus flexible budget operating income.

The sales volume variance is the flexible budget amount minus the static budget amount. A sales volume variance can be calculated for every line on an income statement. The total sales volume variance is the flexible budget operating income minus the static budget operating income. In this problem, the flexible budget amounts are not given and must be calculated. The flexible budget for sales dollars is the static budget amount of $160,000 divided by the static budget sales units of 80,000 and multiplied by the actual sales units of 100,000, which is $200,000. The flexible budget for variable costs is calculated the same way and is $120,000. The fixed cost in the flexible budget is the same as the fixed cost in the static budget: $40,000. The flexible budget operating income is therefore $200,000 ? $120,000 ? $40,000, which equals $40,000. The sales volume variance is the flexible budget operating income of $40,000 minus the static budget operating income of $24,000, which is $16,000. Because the variance is positive on a net income line, it is a favorable variance.

This is the total static budget variance.

This answer results from adjusting the fixed costs in the static budget to a flexible budget amount that reflects the difference between the static budget sales units and the actual sales units. However, fixed costs do not change with changes in sales or manufacturing volume, and so the fixed costs in the flexible budget should be the same as the fixed costs in the static budget.