微信扫一扫

实时资讯全掌握

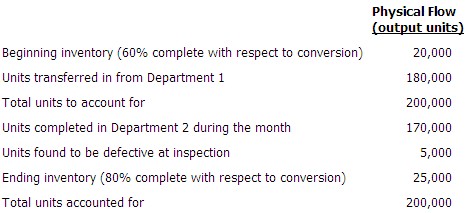

A company employs a process costing system for its two-department manufacturing operation using the first-in, first-out (FIFO) inventory method. When units are completed in Department 1, they are transferred to Department 2 for completion. Inspection takes place in Department 2 immediately before the direct materials are added, when the process is 70% complete with respect to conversion. The specific identification method is used to account for lost units. The number of defective units (that is, those failing inspection) is usually below the normal tolerance limit of 4% of units inspected. Defective units have minimal value, and the company sells them without any further processing for whatever it can. Generally, the amount collected equals, or slightly exceeds, the transportation cost. A summary of the manufacturing activity for Department 2, in units for the current month, is presented below.  Beginning work-in-process inventory was valued at $78,000, consisting of $23,000 of transferred-in costs and $55,000 of conversion costs. Transferred-in costs for units transferred in during the month were $360,000. Costs added to production during the month were $156,000 in direct materials added and $326,700 in conversion costs added. The amount of spoilage cost that was expensed for the month was Beginning work-in-process inventory was valued at $78,000, consisting of $23,000 of transferred-in costs and $55,000 of conversion costs. Transferred-in costs for units transferred in during the month were $360,000. Costs added to production during the month were $156,000 in direct materials added and $326,700 in conversion costs added. The amount of spoilage cost that was expensed for the month wasA. $16,479 B. $0 C. $19,000 D. $16,300 |