This answer results from 1. adding the tax on the gain from the sale of the land to the cash received instead of subtracting it from the cash received, and 2. subtracting the tax benefit on the loss from the sale of the building from the cash received instead of adding it to the cash received. A gain creates an obligation to pay income tax which decreases the net cash flow, while a loss creates a tax benefit because it decreases the amount of income tax due. Therefore, in calculating the net cash flow from the sale of an asset, the tax on a gain should be subtracted from the cash received and the tax benefit of a loss should be added to the cash received.

This answer results from omitting the net cash flow from the sale of the land.

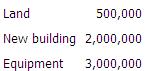

The fifth year's net cash flow would be: Cash flow from operations after tax: ($1,200,000 ? $300,000) × .6 = $540,000 Depreciation tax shield: Depreciation on building = $2,000,000 ÷ 10 = $200,000 per year for 10 years 1 Depreciation on equipment = $3,000,000 ÷ 5 = $600,000 per year for 5 years 1 Total depreciation in Year 5 would be $200,000 + $600,000, or $800,000 2 The depreciation tax shield in Year 5 is $800,000 × .4, or $320,000 Sale of land, net of tax: The land is sold for $800,000 and cost $500,000. Since land is not depreciated, its tax basis is $500,000 (an asset's book value for tax purposes is called its tax basis). There will be a $300,000 gain on the sale that will be taxable at the rate of 40%, which is $120,000. Thus, the net cash flow from the sale of the land will be $800,000 ? $120,000, or $680,000. Sale of building, net of tax: The building is sold for $500,000. Its tax basis at the end of the 5th year is $2,000,000 ? (5 × $200,000) = $1,000,000. Since it is sold for $500,000, there is a loss of $500,000 on the sale. The tax benefit from the loss is $500,000 × .40, or $200,000. The net cash flow from the sale of the building is $500,000 + $200,000 tax benefit from the loss, or $700,000. Sale of equipment, net of tax: The equipment will be fully depreciated at the end of the 5th year. It will be sold for a net amount of $250,000 ($300,000 proceeds from sale minus removal cost of $50,000). The full net amount is taxable, so tax on the gain is $250,000 × .4, or $100,000. The net cash flow from the sale will therefore be $250,000 ? $100,000, or $150,000. Total cash flow for Year 5 is $540,000 cash flow from operations after tax + $320,000 depreciation tax shield + $680,000 sale of land + $700,000 sale of building + $150,000 sale of equipment = $2,390,000. 1For tax purposes, the depreciable base is always 100% of an asset's cost, regardless of which depreciation method is used for tax purposes and regardless of whether salvage value is expected. 2Depreciation on land is not included because land is not depreciated.

This answer results from depreciating the building over a 5 year period instead of over 10 years.

|

Olson uses straight-line depreciation for tax purposes and will depreciate the building over 10 years and the equipment over 5 years.Olson's effective tax rate is 40%. Revenues from the special contract are estimated at $1.2 million annually, and cash expenses are estimated at $300,000 annually. At the end of the fifth year, the assumed sales values of the land and building are $800,000 and $500,000, respectively. It is further assumed the equipment will be removed at a cost of $50,000 and sold for $300,000. As Olson utilizes the net present value (NPV) method to analyze investments, the net cash flow for period 5 would be

Olson uses straight-line depreciation for tax purposes and will depreciate the building over 10 years and the equipment over 5 years.Olson's effective tax rate is 40%. Revenues from the special contract are estimated at $1.2 million annually, and cash expenses are estimated at $300,000 annually. At the end of the fifth year, the assumed sales values of the land and building are $800,000 and $500,000, respectively. It is further assumed the equipment will be removed at a cost of $50,000 and sold for $300,000. As Olson utilizes the net present value (NPV) method to analyze investments, the net cash flow for period 5 would be