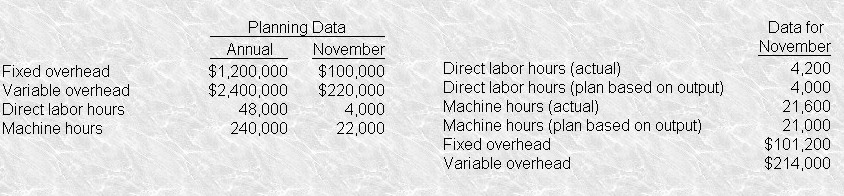

Answer (D) is correct . The fixed overhead volume (production volume or idle capacity) variance is the difference between budgeted fixed costs and the product of the standard fixed overhead cost per unit of input and the standard units of input allowed for the actual output. Budgeted fixed costs for the month were $100,000. The standard cost of actual output was $105,000 [21,000 machine hours planned for actual output ¡Á ($1,200,000 planned annual FOH ¡Â 240,000 planned annual machine hours) FOH application rate]. Hence, the fixed overhead volume variance was $5,000 favorable. It was favorable because the budget for fixed overhead was less than the amount applied to jobs. An overapplication of fixed overhead suggests that output exceeded expectations.Answer (A) is incorrect because The variance was favorable.

Answer (B) is incorrect because The variance was favorable.

Answer (C) is incorrect because The amount of $10,000 is based on 22,000 planned machine hours.

|

Nanjones’ fixed overhead volume variance for November was

Nanjones’ fixed overhead volume variance for November was