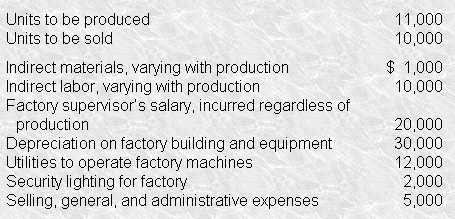

Answer (A) is correct . Variable overhead consists of those inputs to the production process that (1) vary with the level of production and (2) cannot be practicably traced to end products. In Valley’s case, these include indirect materials ($1,000), indirect labor ($10,000), and utilities ($12,000), for a total of $23,000. Dividing this amount by the number of units scheduled for production yields a variable overhead application rate of $2.09 ($23,000 ÷ 11,000).

|