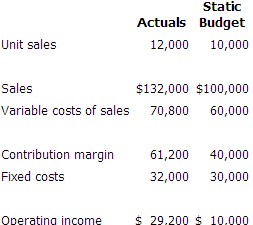

题干:Clear Plus公司制造和销售口袋保护盒,5月份静态预算和实际结果如下

下列哪一项关于公司5月份分析师正确的

A.弹性预算变动成本差异是10800美元不利。

B.销售价格差异是32000美元有利。

C.弹性的预算差额8,000元有利。

D.销量差异8,000元有利。

考点:Cost and Variance Measures-Sales Variances

关键词:variance

解题思路:分别验证ABCD

| DM | Price variance | =(AP-SP)*AQ | | | |

| (spending variance) | | | | |

| | | Mix variance | =ATQ*(AM-SM)*SP | =ATQ*AM*SP-ATQ*SM*SP |

| | | 实际总投入量中,原材料投入的实际比重和标准比重的差异,加权平均。 |

| Quantity variance | =(AQ-SQ)*SP=(AQ*AM-SQ*SM)*SP | | | |

| (efficiency variance) | (SQ= acutal output*standard input per unit) | yield variance | =(ATQ-STQ)*SM*SP | =ATQ*SM*SP-STQ*SM*SP |

| | | | 在原材料比重没有变化的情况下,实际投入量和标准投入量的差异。 | |

| DL | Price variance | =(AR-SR)*ADLH | | | |

| | (spending variance) | | | | |

| | | | Mix variance | =ATDLH*(AM-SM)*SP | =ATDLH*AM*SP-ATDLH*SM*SP |

| | | | 实际投入人工小时数中,各种人工的实际比重和标准比重的差异,加权平均。 |

| | Quantity variance | =(ADLH-SDLH)*SR | | | |

| | (efficiency variance) | SDLH= acutal output*standard DLH per unit) | yield variance | =(ATDLH-STDLH)*SM*SP | =ATDLH*SM*SP-STDLH*SM*SP |

| | | | 在人工投入比重没有变化的情况下,实际投入人工小时数和标准投入人工小时数的差异。 |

| VOH

(assum VOH is applied based on DLH) | Price variance | =(AR-VPOHR)*ADLH | | | In the standard cost system: Applied VOH=Flexible budget

VOH,

Applied FOH≠Flexible budget FOH |

| (spending variance) | =Actual VOH-ADLH*VPOHR | | |

| | VPOHR=Budgeted total VOH/

Bugeted allocation base(DLH) | |

| | | | |

| Quantity variance | =(ADLH-SDLH)*VPOHR | | |

| (efficiency variance) | | | |

| FOH | Spending variance | =Budgeted FOH-Actual FOH | | |

| | | | |

| | | | |

| Production volumn variance | =Budgeted FOH-applied FOH | | |

| (uncontrollable) | (Applied FOH=

FPOHR*standard activity per unit*actual output) |

| | =FPOHR*(DH-SH) | | |

| | (DH=Denominator

hours,SH=standard hours allowed for actual output) |

| | | | | |

| Sales | Price variance | =(AP-BP)*AS | | | |

| | | | | |

| | | | | |

| Sals volumn variance | =(AS-BS)*BCM per unit | Mix variance | =ATS*(AM-BM)*BCM per unit | =ATS*(AM-BM)*BCM per unit |

| (BCM per unit=BP-BVC) | 总销售额下,各产品售出的预算比重和实际比重的差异,加权平均 | |

| | | |

| Quantity variance | =(AS-BS)*BM*BCM per unit | (Market size and market share) |

| Uncontrollable | 在销售产品比重未发生变化的情况下,实际销售额与预算销售额的差异 |

To answer such a question we have to solve for each possible suggested statement. It is better to start with the easiest ones. The flexible budget variable cost variance is the difference between actual variable costs and the flexible budget variable costs. The actual variable cost is given as $70,800. The flexible budget variable cost is calculated as the standard unit variable cost multiplied by the actual level of sales volume, which was 12,000. We can calculate the standard unit variable cost using the static (master) budget figures given: $60,000 ÷ 10,000 = $6.00. So the flexible budget variable cost is $6.00 × 12,000 = $72,000. The flexible budget variable cost variance thus is $1,200 favorable ($70,800 ? $72,000). So this is not a correct statement.

To answer such a question we have to solve for each possible suggested statement. It is better to start with the easiest ones. The sales price variance measures the impact of the difference caused by a variance in price. When it is not specified what item's sales price variance is referred to, we can assume the contribution margin. The sales price variance for the contribution margin is calculated as follows: (Actual Contribution per unit ? Standard Contribution per unit) × Actual Quantity. Actual contribution per unit is $5.10 ($61,200 ÷ 12,000), and the standard contribution margin is $4.00 ($40,000 ÷ 10,000). The actual quantity is 12,000. The sales price variance is therefore $13,200 favorable: ($5.10 ? $4.00) × 12,000. So this statement is not correct.

To answer such a question we have to solve for each possible suggested statement. It is better to start with the easiest ones. When it is not otherwise specified, the flexible budget variance equals the difference between actual operating income and the flexible budget operating income. The flexible budget contribution margin equals actual units times standard contribution margin or $48,000 ($4.00 standard contribution margin × 12,000 actual quantity). Fixed costs in the flexible budget are the same as fixed costs in the static budget. Therefore, the flexible budget operating income equals flexible budget contribution margin less the master budget (static budget) fixed costs: $18,000 ($48,000 ? $30,000). Now we can determine the flexible budget variance as $11,200 favorable: ($29,200 ? $18,000). So this statement is not correct.

To answer such a question we have to solve for each possible suggested statement. It is better to start with the easiest ones. The sales volume variance measures the impact of difference between actual sales volume and budgeted sales volume. When it is not specified what item's sales volume variance is referred to, we can assume the contribution margin. The sales volume variance is calculated as follows: (Actual Sales Volume ? Budgeted Sales Volume) × Standard Contribution per Unit. The actual quantity was 12,000 and the standard quantity was 10,000. The standard contribution per unit is $4.00 ($40,000 ÷ 10,000). The sales volume variance is therefore $8,000 favorable: (12,000 ? 10,000) × $4.00. The variance is favorable as the actual quantity of units sold is greater than budgeted. So this statement is correct.