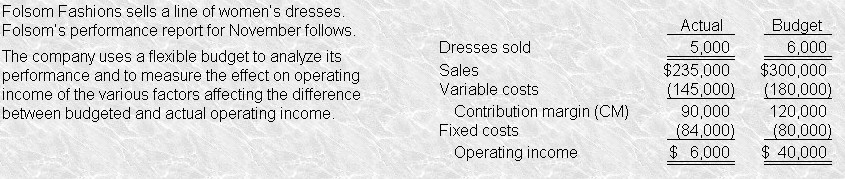

Answer (D) is correct . The sales price variance is the actual number of units sold (5,000), times the difference between budgeted selling price ($300,000 ¡Â 6,000) and actual selling price ($235,000 ¡Â 5,000). ($50 - $47) x 5,000 = $15,000 U

Answer (A) is incorrect because The difference between the actual and budgeted contribution margins is $30,000.

Answer (B) is incorrect because The difference between actual and budgeted unit sales times the actual unit CM equals $18,000.

Answer (C) is incorrect because The sales quantity variance is $20,000.

Answer (B) is incorrect because The difference between actual and budgeted unit sales times the actual unit CM equals $18,000.

Answer (C) is incorrect because The sales quantity variance is $20,000.