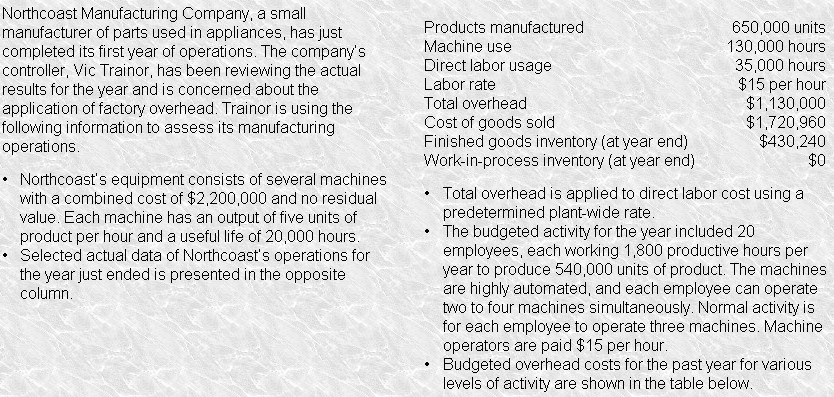

题干:Northcoast 制造企业是一家生产器械零部件的公司。刚刚运营一年。公司财务总监 Vic 在审核过去一年的实际运营状况时对车间期间费用分配感到担忧。Vic使用右列数据来评估公司制造情况

Northcoast 公司的设备包含几个机器, 成本共2.2m且没有残值。每一个机器都能每小时产5个产品和20k的工时寿命。Northcoast 选取年末运营数据如下

所有期间费用按照全厂统一费用率和人工工时分配。

预算作业包括20个工人,每一个工人全年工作1800小时共生产540k件产品。机器高度自动化,每一个工人可以同时操作2-4个机器。通常情况下每一个工人可以操作3台机器,机器操作工人工资是15/小时

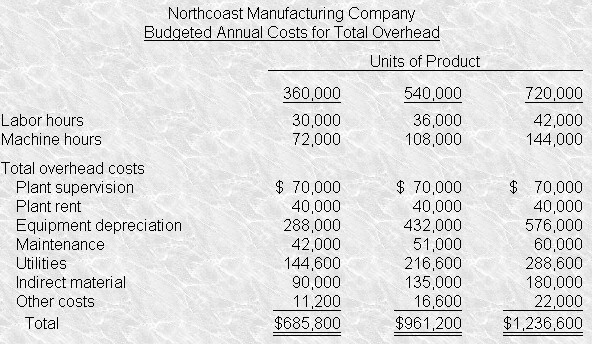

不同作业水平下预算期间费用如下表

问Northcoast 期间费用是多分摊还是少分摊

考点:Cost Allocation Techniques-Overhead Allocation and Normal Costing -- Calculations

关键词:overhead predetermined plant overhead labor cost

解题思路:首先要确定统一费用率=961000/(36000*15)=1.78

按照实际人工成本分配标准费用=(15*35,000hours)*1.78=9345000

差异=9345000-113000=195000underapplied

Answer (D) is correct . The amount of overhead overapplied/underapplied is found by subtracting the actual incurred overhead from the actual applied overhead. The actual incurred overhead from the actual applied overhead.The actual applied overhead is $934,5000[($15*35,000hours)*1.78].Thus,the amount of underapplied overhead is $195,000($934,500-$1,130,000)

Answer (A) is incorrect because The figure of $195,500 is the amount underapplied.

Answer (B) is incorrect because The figure of $168,800 results from subtracting actual incurred overhead from total budget overhead.

Answer (C) is incorrect because The figure of $168,800 results from subtracting actual incurred overhead from total budget overhead.