微信扫一扫

实时资讯全掌握

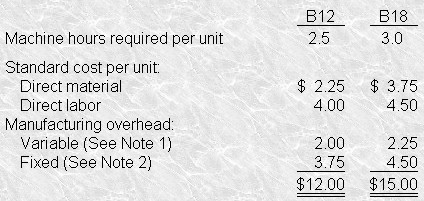

Stewart Industries has been producing two bearings, components B12 and B18, for use in production.  Stewart’s annual requirement for these components is 8,000 units of B12 and 11,000 units of B Recently, Stewart’s management decided to devote additional machine time to other product lines resulting in only 41,000 machine hours per year that can be dedicated to the production of the bearings. An outside company has offered to sell Stewart the annual supply of the bearings $11.25 for B12 and $13.50 for B18 Stewart wants to schedule the otherwise idle 41,000 machine hours to produce bearings so that the company can minimize its costs (maximize its net benefits). Note 1:? Variable manufacturing overhead is applied on the basis of direct labor hours. Note 2:? Fixed manufacturing overhead is applied on the basis of machine hours.Assume that Stewart’s idle capacity of 41,000 machine hours has a traceable avoidable annual fixed cost of $44,000 that will continue if the capacity is not used. The maximum price Assume that Stewart’s idle capacity of 41,000 machine hours has a traceable avoidable annual fixed cost of $44,000 that will continue if the capacity is not used. The maximum price Stewart would be willing to pay a supplier for component B18 is Stewart’s annual requirement for these components is 8,000 units of B12 and 11,000 units of B Recently, Stewart’s management decided to devote additional machine time to other product lines resulting in only 41,000 machine hours per year that can be dedicated to the production of the bearings. An outside company has offered to sell Stewart the annual supply of the bearings $11.25 for B12 and $13.50 for B18 Stewart wants to schedule the otherwise idle 41,000 machine hours to produce bearings so that the company can minimize its costs (maximize its net benefits). Note 1:? Variable manufacturing overhead is applied on the basis of direct labor hours. Note 2:? Fixed manufacturing overhead is applied on the basis of machine hours.Assume that Stewart’s idle capacity of 41,000 machine hours has a traceable avoidable annual fixed cost of $44,000 that will continue if the capacity is not used. The maximum price Assume that Stewart’s idle capacity of 41,000 machine hours has a traceable avoidable annual fixed cost of $44,000 that will continue if the capacity is not used. The maximum price Stewart would be willing to pay a supplier for component B18 isA. $10.50 B. $14.00 C. $14.50 D. Some amount other than those given. |