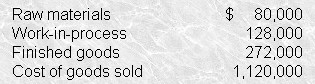

Answer (C) is correct . Given the amounts involved, $133,000 is material; thus, over- or underapplied overhead should be allocated to all work-in-process, finished goods, and cost of goods sold. The proportion of the total of these three accounts represented by cost of goods sold is 73.68% [$1,120,000 ¡Â ($128,000 + $272,000 + $1,120,000)]. The amount of underapplied overhead assigned to cost of goods sold is thus $98,000 ($133,000 ¡Á 73.68%), making the total reported amount of cost of goods sold $1,218,000 ($1,120,000 + $98,000)

Answer (A) is incorrect because The amount of $987,000 results from improperly subtracting the entire amount of underapplied overhead from the balance of cost of goods sold instead of allocating it across three inventory accounts.

Answer (B) is incorrect because The amount of $1,213,100 improperly includes raw materials in the allocation base for underapplied overhead.

Answer (D) is incorrect because The amount of $1,253,000 results from improperly allocating the entire amount of underapplied overhead to cost of goods sold.

The company’s underapplied overhead equals $133000, On the basis of this information, Elk’s cost of goods sold is most appropriately reported as

The company’s underapplied overhead equals $133000, On the basis of this information, Elk’s cost of goods sold is most appropriately reported as