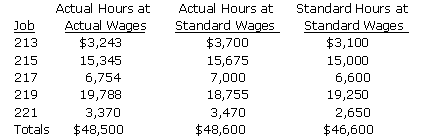

A. This is the difference between the Actual Hours at Standard Wages and Standard Hours at Standard Wages. This is the direct labor efficiency variance. The formula for the direct labor efficiency variance is (AQ - SQ) × SP. That formula can also be written as (AQ × SP) - (SQ × SP). (AQ × SP) is equal to "Actual Hours at Standard Wages," while (SP × AQ) is equal to "Standard Hours at Standard Wages." The direct labor efficiency variance is one component of the total flexible budget direct labor variance. The other component is the direct labor rate variance. However, the question asks for the total flexible budget direct labor variance.

B. The flexible budget variance is unfavorable, because the actual cost incurred is greater than the standard cost for the actual level of output (the flexible budget).

C. This is the difference between the Actual Hours at Actual Wages and Actual Hours at Standard Wages. This is the direct labor rate variance. The formula for the direct labor rate variance is (AP - SP) × AQ. That formula can also be written as (AP × AQ) - (SP × AQ). (AP × AQ) is equal to "Actual Hours at Actual Wages," while (SP × AQ) is equal to "Actual Hours at Standard Wages." The direct labor rate variance is one component of the total flexible budget direct labor variance. The other component is the direct labor efficiency variance. However, the question asks for the total flexible budget direct labor variance.

D. The total labor variance (also called the flexible budget variance) is the difference between the actual costs incurred by the company and the standard costs for the actual level of output (the flexible budget). The "Actual Hours at Actual Wages" in the first column are the actual costs incurred. The "Standard Hours at Standard Wages" in the third column are the standard costs for the actual level of output. Thus, the total labor variance is $48,500 - $46,600 = $1,900 unfavorable.