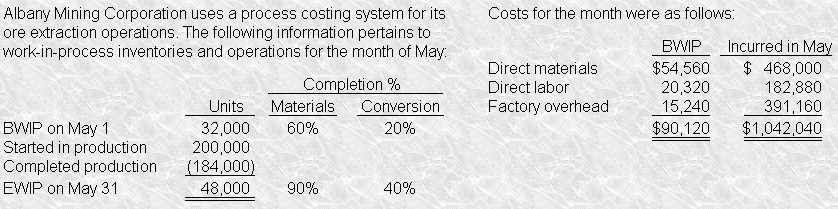

Answer (A) is correct . The FIFO equivalent units of conversion cost equal 196,800. Conversion cost incurred during May was $574,040 ($182,880 DL + $391,160 FOH). Hence, the equivalent-unit conversion cost under FIFO is $2.92 ($574,040 ¡Â 196,800). 1968000=32000*0.8+48000*0.4+152000=196800

Answer (B) is incorrect because The cost per equivalent unit under the weighted-average method is $3.00.

Answer (C) is incorrect because Total conversion cost divided by FIFO equivalent units of conversion cost equals $3.10.

Answer (D) is incorrect because The amount of $3.23 assumes EWIP is 0% complete as to conversion cost.

Using the FIFO method, Albany Mining’s equivalent unit conversion cost for May is

Using the FIFO method, Albany Mining’s equivalent unit conversion cost for May is